Introduction

Picture this: your mother needs dialysis three times a week, and each round trip to the treatment center costs $45 in professional transport fees. Over the course of a year, that's nearly $7,000 in medical transportation costs alone. Many families facing this reality don't know they may be able to deduct part of these costs through medical transportation tax deductions.

The IRS allows qualified medical transportation costs to be deducted as part of your medical expenses. Specific rules govern what qualifies, who can claim it, and how much you can actually deduct. You must itemize rather than take the standard deduction, and only unreimbursed costs exceeding 7.5% of your adjusted gross income count.

This guide covers:

- Which transportation modes qualify

- How the 7.5% AGI threshold works

- How to calculate your deduction using the IRS mileage rate

- What expenses don't qualify

- How to document and file correctly

TLDR: Medical Transportation Tax Deductions at a Glance

- You must itemize deductions on Schedule A (Form 1040) — only about 10% of taxpayers do this since the standard deduction is often higher

- Only unreimbursed costs exceeding 7.5% of your adjusted gross income (AGI) are deductible

- Qualifying transport includes personal vehicles (21 cents/mile for 2024–2025), buses, taxis, planes, ambulances, and NEMT services like wheelchair vans

- Parking fees, tolls, and companion travel costs also qualify

- Keep detailed records — mileage logs, receipts, and medical necessity documentation are all required

What Counts as a Deductible Medical Transportation Expense?

The IRS defines deductible medical transportation as costs "primarily for and essential to medical care," which includes trips for diagnosis, treatment, prevention of illness, or therapy for physical or mental conditions. This definition comes directly from IRS Publication 502, the authoritative guide on medical and dental expense deductions.

IRS-Approved Transportation Modes:

- Bus, taxi, train, and plane fares

- Ambulance services

- Professional non-emergency medical transportation (NEMT) — including wheelchair van transport, stretcher transport, and other medically adapted vehicles

Patients who use licensed NEMT providers like AllCare Medical Transport for recurring trips to dialysis, chemotherapy, rehabilitation, or specialist appointments can include those costs as deductible transportation expenses.

If you drive yourself or a family member to appointments, personal vehicle costs qualify too.

Personal Vehicle Use:

You can deduct car expenses using one of two methods:

- Standard mileage rate: 21 cents per mile for both 2024 and 2025 tax years

- Actual expenses: Out-of-pocket costs for gas and oil only — not depreciation, insurance, or general maintenance

Choose whichever method yields the higher deduction. Parking fees and tolls are deductible regardless of which method you choose, added on top of mileage or actual expenses.

Companion Travel:

The IRS allows deductions for companion transportation when medically necessary:

- A parent accompanying a child who needs medical care

- A caregiver traveling with a patient unable to travel alone

- A nurse giving injections or medications during transport

The companion's transportation costs (mileage, fares, parking, tolls) qualify just like the patient's expenses.

Who Can Claim the Medical Transportation Tax Deduction?

You can deduct qualifying transportation costs for yourself, your spouse, and your dependents.

The IRS defines two dependent categories: qualifying children (under 19, or under 24 if a full-time student) and qualifying relatives who meet income and support tests. For 2024, a qualifying relative must have gross income under $5,050.

The Itemization Requirement

This deduction is only available if you itemize on Schedule A instead of taking the standard deduction. For 2024, standard deduction amounts are:

- Single or Married Filing Separately: $14,600

- Married Filing Jointly or Qualifying Surviving Spouse: $29,200

- Head of Household: $21,900

If your total itemized deductions (medical expenses, mortgage interest, charitable contributions, state taxes) don't exceed your standard deduction, itemizing won't benefit you. Only about 10% of taxpayers itemized in tax year 2022 after the Tax Cuts and Jobs Act increased standard deductions.

The 7.5% AGI Threshold

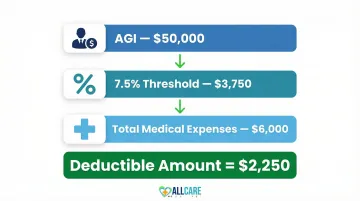

Only medical expenses exceeding 7.5% of your adjusted gross income (AGI) are deductible. Here's how it works:

- AGI: $50,000

- 7.5% threshold: $3,750

- Total medical expenses (including transportation): $6,000

- Deductible amount: $2,250 ($6,000 - $3,750)

You must clear this threshold before any medical expenses become deductible.

Transportation usually makes up a smaller share of total medical expenses than premiums, prescriptions, and out-of-pocket bills — but it still counts toward clearing that threshold.

How to Calculate Your Medical Transportation Deduction

Step 1: Tally All Qualifying Medical Transportation Costs

Add up every qualifying trip for the tax year:

- Professional transport service fees (NEMT, ambulance)

- Personal vehicle mileage or actual gas/oil expenses

- Parking fees and tolls

- Public transportation fares (bus, train, taxi, plane)

- Companion travel costs

Combine these with all other qualifying medical expenses (insurance premiums, prescriptions, copays, dental work, vision care).

Step 2: Calculate Your 7.5% AGI Floor

Multiply your adjusted gross income (line 11 of Form 1040) by 0.075. Only expenses above this amount are deductible.

Step 3: Choose Your Vehicle Expense Method

If you drove your personal vehicle, calculate both methods and use the higher amount.

Method A — Standard Mileage Rate:

- Total medical miles driven × the IRS medical mileage rate (21 cents/mile for 2024 — verify the current rate for your tax year)

- Add parking fees and tolls

Method B — Actual Expenses:

- Add up all gas and oil receipts for medical trips

- Add parking fees and tolls

Worked Example

Jane has an AGI of $60,000. She drove 2,000 miles for medical appointments ($420 at the standard rate), paid $150 in parking, and used a wheelchair van service 24 times at $45 per trip for dialysis ($1,080). Her total transportation costs come to $1,650.

Add $3,000 in other medical expenses (insurance premiums, prescriptions) for a combined total of $4,650.

- 7.5% AGI floor: $60,000 × 0.075 = $4,500

- Amount above the floor: $4,650 − $4,500 = $150 deductible

In this scenario, Jane qualifies for only a $150 deduction — a reminder that the AGI floor significantly limits who actually benefits from itemizing medical expenses.

The Reimbursement Rule

Only unreimbursed expenses count toward your deduction. If Medicare, Medicaid, private insurance, or any other source covered the transportation cost, subtract that reimbursement before calculating your total. Mixing reimbursed and out-of-pocket amounts is one of the most common errors on Schedule A.

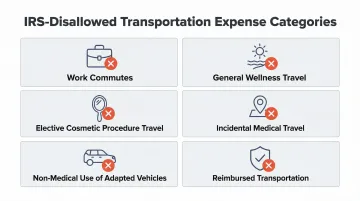

Transportation Costs That Are NOT Tax Deductible

Even with a legitimate medical condition, certain transportation costs never qualify for a deduction. The IRS disallows these categories regardless of circumstance:

- Work commutes — Transportation to and from your job is always a personal expense, even if your condition requires a specially equipped vehicle

- General wellness travel — Trips to a warm climate recommended by a doctor, meditation retreats, or similar "health improvement" outings don't meet the IRS standard of specific medical diagnosis, treatment, or therapy

- Elective cosmetic procedure travel — Transportation to cosmetic surgery is excluded unless the procedure is reconstructive following disease, injury, or congenital defect

- Incidental medical travel — Trips where medical care is a secondary purpose, not the primary reason for the journey

- Non-medical use of adapted vehicles — Operating a specially equipped vehicle for everyday errands doesn't convert those miles into a medical expense

- Reimbursed transportation — Any costs already covered by insurance or a government program cannot be deducted again

How to Claim and Document Medical Transportation Deductions

Filing Process:

Report all medical and dental expenses on Schedule A (Form 1040), Line 1. The form automatically calculates the 7.5% AGI floor and determines your deductible amount. Keep records that support your claim in case of an IRS audit.

Required Documentation:

For Personal Vehicle Use:

Maintain a detailed mileage log with:

- Date of each trip

- Starting point and destination

- Medical purpose (appointment type, provider name)

- Odometer readings (start and end)

- Total miles

For Professional Transport Services:

Keep all receipts and invoices showing:

- Provider name (such as AllCare Medical Transport)

- Date of service

- Pickup and drop-off locations

- Cost per trip

- Type of service (ambulatory, wheelchair, stretcher)

Most professional NEMT providers issue itemized billing statements you can use directly for tax filing.

For All Transportation:

Document medical necessity with:

- Appointment confirmations

- Physician referrals or orders

- Treatment schedules (dialysis, chemotherapy, therapy sessions)

Record Retention:

Keep all medical expense records for 3 years from the date you filed your return or 2 years from the date you paid the tax, whichever is later. Store receipts, mileage logs, and supporting documentation together in case of audit.

Should You Itemize?

Itemizing is worth it only when your total deductions exceed the standard deduction. A few quick checks before you file:

- Add up all itemized deductions, not just medical costs

- Compare that total to your standard deduction amount

- Consult a tax professional if transportation costs are substantial or your situation is complex

Frequently Asked Questions

Is transportation to and from medical appointments tax deductible?

Yes, transportation to and from qualifying medical appointments is deductible as a medical expense — but only if you itemize deductions, your total medical expenses exceed 7.5% of AGI, and the transportation is primarily for medical care.

Can you claim mileage to and from a doctor?

Personal vehicle mileage to and from medical facilities can be claimed using either the IRS standard rate of 21 cents per mile (2024-2025) or actual out-of-pocket gas and oil expenses. Parking fees and tolls are deductible with either method.

What transportation expenses are tax deductible?

IRS-approved transportation includes personal vehicles (mileage or actual costs), bus, taxi, train, plane, ambulance, and professional medical transport such as wheelchair vans. Parking fees, tolls, and qualifying companion travel also count.

Is transportation 100% deductible?

No. Only the unreimbursed portion contributing to total medical expenses exceeding 7.5% of AGI is deductible, and only if you itemize instead of taking the standard deduction. Most taxpayers can deduct only a fraction of their transportation costs.

What is the IRS medical travel rate?

The standard medical mileage rate is 21 cents per mile for both 2024 and 2025 tax years. The IRS adjusts this rate annually, typically announcing changes in December. Always use the rate for the year in which the travel occurred.

What cannot be claimed as a medical expense?

Non-qualifying expenses include reimbursed costs, cosmetic procedure travel, commuting to work, trips for general health improvement, non-prescription medications, and personal care items. See IRS Publication 502 for the complete list.